SMM March 28 News

As of March 28, the most-traded SHFE zinc contract closed at 23,770 yuan/mt, up 345 yuan/mt for the month, a gain of 1.47%. Zinc prices fell throughout March, hitting a low of 23,470 yuan/mt at the beginning of the month and again at month-end. Overall, zinc prices rose significantly in March. Will the upward trend continue in April?

Macro perspective. Internationally in March, Trump escalated tariff policies, with the US expected to impose additional tariffs on copper imports. The auto tariffs took effect on April 2, sparking concerns of a global manufacturing slowdown and dampening risk appetite, putting pressure on non-ferrous metal prices. Domestically, the Two Sessions were held, and aside from the 1.3 trillion yuan in special government bonds, the policies were largely in line with market expectations, including GDP growth of around 5%, a fiscal deficit ratio of about 4%, and a moderately accommodative monetary policy with timely RRR and interest rate cuts. Overall, domestic policies remained favorable. In April, Trump may implement reciprocal tariff policies, raising concerns about the future economy.

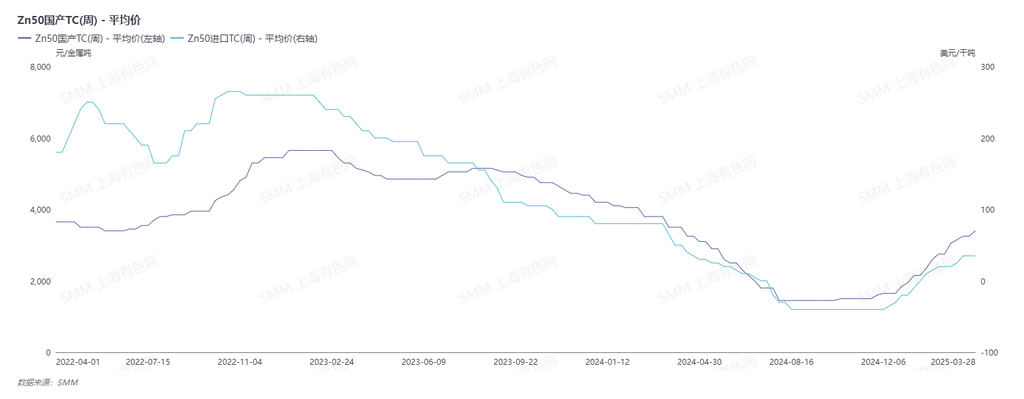

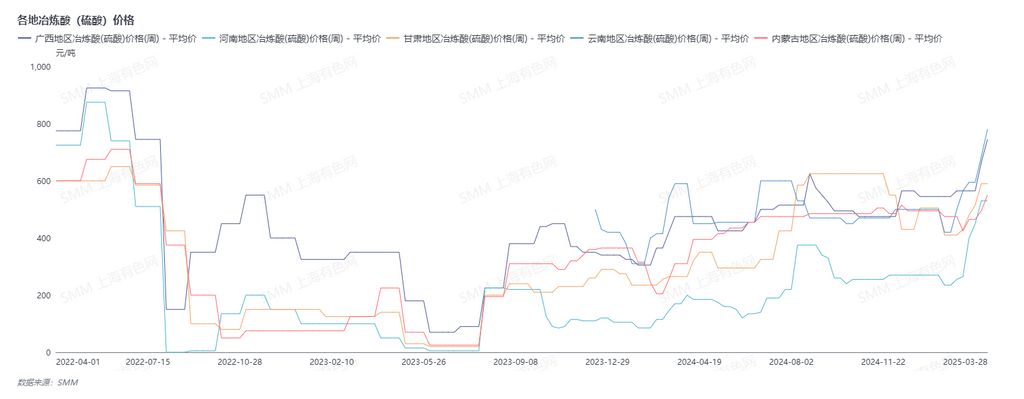

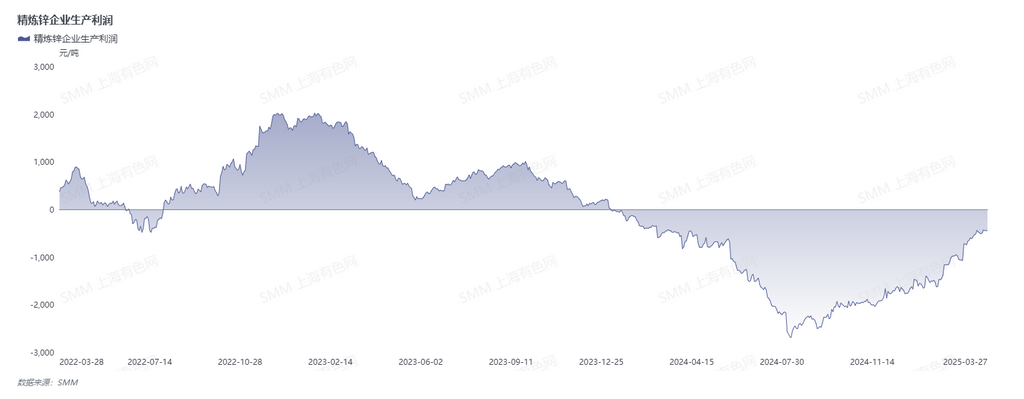

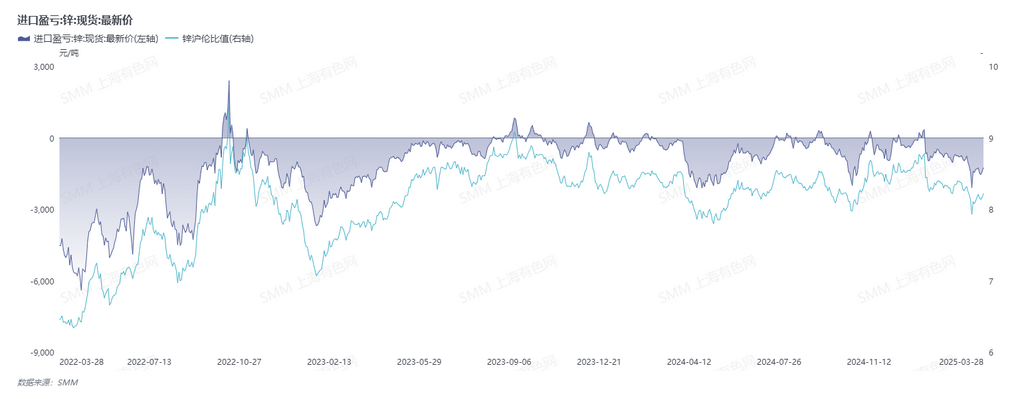

Supply side. In March, as domestic TCs rose above 3,400 yuan/mt (metal content) and sulphuric acid prices increased again, smelters became more motivated to produce, delaying maintenance and increasing production. However, the import window for zinc ingots remained closed throughout March, and the inflow of imported zinc ingots may have decreased, resulting in no significant increase in overall zinc ingot supply. Social inventories remained around 130,000 mt. In April, smelter profits are expected to improve, boosting production motivation and further delaying routine maintenance. Additionally, new capacity in Henan is expected to start production, with zinc ingot output likely in May, potentially leading to a significant increase in zinc ingot supply.

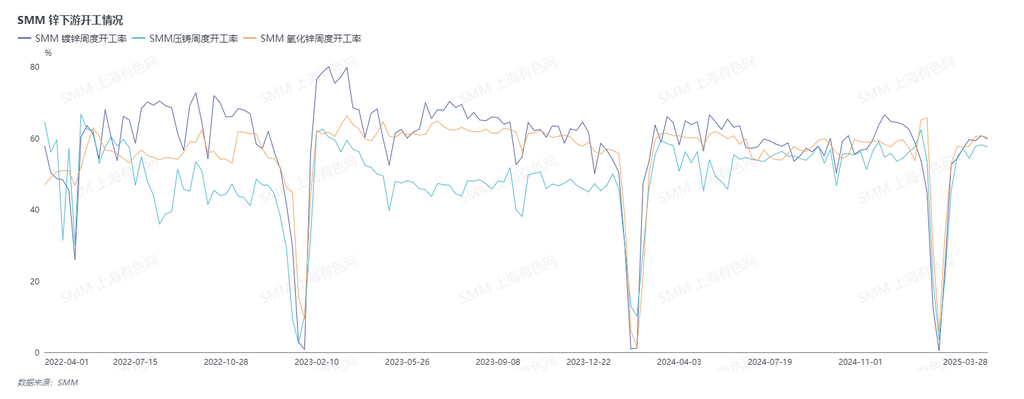

Demand side. In March, as end-users gradually resumed operations, domestic zinc downstream enterprises restarted production. Galvanizing operations were slightly lower than the same period last year, with limited actual market consumption recovery. However, steel towers and some export orders performed well. Die-casting zinc alloy plants showed a polarization, with orders more concentrated in larger plants, and overall operations were better than the same period last year. Zinc oxide performance remained stable. Domestically, local government bond issuance progressed rapidly, and the Ministry of Finance's "2024 China Fiscal Policy Implementation Report" released on March 24 explicitly mentioned actively expanding effective investment, focusing on key areas and weak links, and accelerating the issuance of government bonds to form physical workloads as soon as possible. There is still a good expectation for subsequent project implementation. Power investment continues to increase, and the auto industry is boosted by the trade-in policy. Domestic zinc downstream consumption is expected to continue recovering in April.

Looking ahead to April, overall supply is expected to turn loose, while demand, though expected to improve, remains limited. Continued attention is needed on macro guidance and domestic consumption.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided is for reference only. This article does not constitute direct investment research advice. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.)